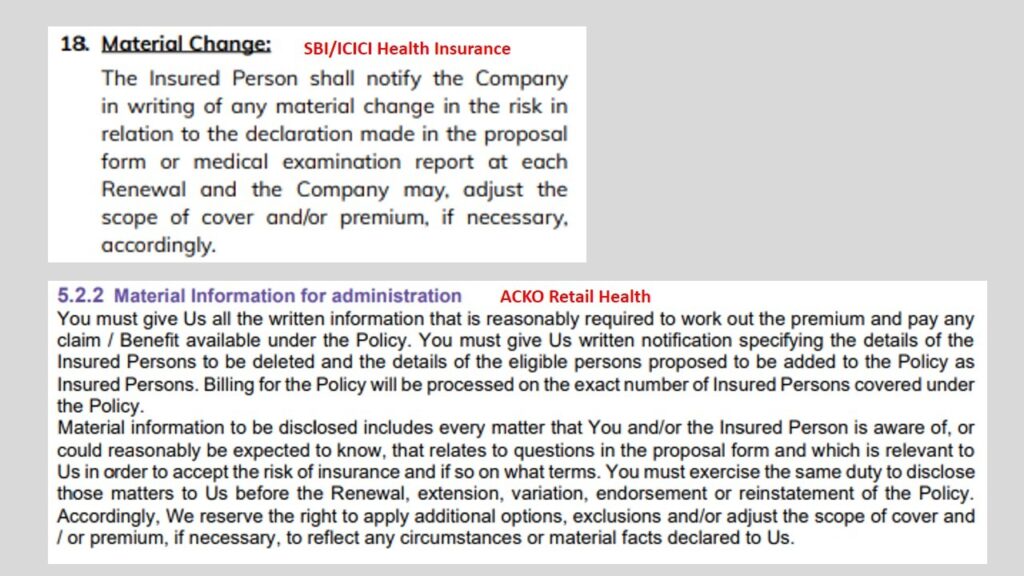

There is growing concern among policyholders as well as prospective buyers regarding the “material change” clauses found in certain health insurance policies. The exact wording of this clause in SBI, ICICI Lombard, and Acko Health Insurance policies is shown in the image below.

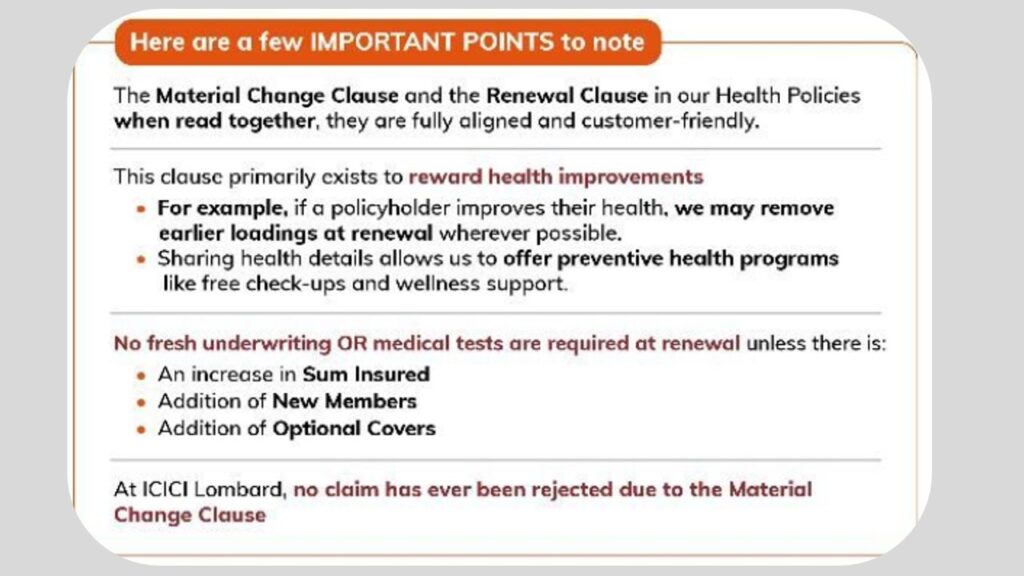

After several insurance distributors raised questions about this condition, ICICI Lombard issued a clarification. According to them, the clause is intended to reward health improvements and does not require fresh underwriting.

They also claim that there is no need for policyholders to notify the company if they renew without changing the sum insured, members, or optional covers. However, this clarification should be taken with a pinch of salt, as it is difficult to fully believe.

No other insurer besides ICICI Lombard has issued any clarification, even though the issue has been widely discussed in the media.

What should you do?

As far as ICICI’s clarification is concerned, it feels more like a cover-up for the damage already done to their reputation. The clause itself is vague, and nowhere does it explicitly state what ICICI is now trying to explain.

Acko’s wording is even more concerning and can definitely be used against policyholders if they are diagnosed with a disease especially a chronic one. Regardless of any explanation from these insurers, the very inclusion of such a clause indicates that they are looking for ways to distance themselves from policyholders diagnosed with chronic illnesses, which can lead to continuous high-value claims that insurers find difficult to handle.

This clause seems like an attempt to bypass the IRDAI condition that, for individual products, insurers cannot load renewal premiums based on an individual policyholder’s claim experience.

With no scope to increase premiums due to this IRDAI guideline, insurance companies appear to be looking for disguised ways to justify premium hikes.

There are only three conditions where insurance companies can resort to fresh underwriting on renewal of policy, means can ask the disclosure of such information. These are :

- Increase in sum insured

- Addition of new member to policy or

- Choosing an optional cover

Asking the policyholders to disclose material risk at the time of renewal without any of the above three conditions is not allowed as per IRDAI norms.

People who have health insurance policies with such condition should seriously consider porting to other insurance products. The inclusion of such a clause is, in itself, lack of transparency, as the insurer is hiding behind vague language to either hike your premium or restrict your future claims.

No amount of clarification should be blindly trusted, and it is always better to avoid such policies.