Energy Policy by HDFC ERGO is a health insurance special plan for individuals already living with chronic lifestyle conditions such as Type 1 Diabetes, Type 2 Diabetes Mellitus, Impaired Fasting Glucose (IFG), Impaired Glucose Tolerance (IGT), and Hypertension. Recognizing the long-term medical needs and potential complications associated with these conditions, the policy offers coverage of up to 50 lakh, ensuring strong financial protection against rising healthcare costs.

Positive Highlights of the Policy

AYUSH (Ayurveda, Yoga & Naturopathy, Unani, Siddha, and Homoeopathy) treatments are covered up to the full cover limit without any restrictions, unlike many other policies where prior approval may be required for yoga or naturopathy.

Pre- and post-hospitalization expenses on consultation, diagnostics, medicines etc are covered for 30 and 60 days respectively, with no limitations other than the time period specified.

Organ donor expenses are also covered, and the benefit is not limited only to kidney transplants, unlike the Star Health Diabetes Safe policy.

Additionally, the policy provides a private room entitlement during hospitalization. If you choose a shared room instead of private room, the policy also covers non-medical expenses such as Admission/registration charges, Hospital administrative charges, Consumables such as – Gloves, masks etc. that are typically excluded under most health insurance plans.

If the coverage limit is exhausted during the policy period due to claims, the policy automatically restores the cover once. This restored amount can be used for any illness, regardless of whether a claim for the same condition was made earlier. Many other policies restrict the use of restored cover for previously claimed illnesses, but this policy has no such limitation.

You have the option to choose a co-payment feature, where you pay a certain percentage of each claim in exchange for a lower policy premium. However, I would advise against opting for this feature, as it can lead to significant out-of-pocket expenses at the time of a claim.

Policy has a comprehensive Wellness Program designed especially for individuals with diabetes or hypertension. It encourages regular monitoring through two scheduled check-ups each year, covering key parameters like HbA1c, blood pressure, BMI, cholesterol, ECG, and doctor consultations. These results are converted into points, which can earn you significant renewal benefits up to 25% discount on next year’s premium along with reimbursement for healthcare expenses. In the Gold Plan, the insurer even pays for or reimburses the check-up costs, making participation convenient.

Policy has a bonus feature, it adds 10% of cover limit on each renewal that too irrespective of claim in policy. You can double the coverage limit using this feature. Most of the insurance policy which provide this feature, reduce the bonus on account of claim in any policy or do not accrue the bonus if claim has occurred in policy.

The policy clearly states how it will handle any disease or health condition that existed before purchase but was not disclosed. While most insurers only reject claims or cancel the policy for non-disclosure, HDFC ERGO also outlines additional options—such as permanently excluding the condition, covering it with a waiting period, or applying a loading. These alternatives are clearly mentioned in the policy, which is uncommon in many other health insurance plans.

All health insurance policies have a list of specific diseases that are covered after a waiting period usually two years because these conditions can develop gradually and may not be known at the time of purchase. Many policies mention only broad categories like ‘ENT disorders,’ which creates confusion since many illnesses can fall under that system. This can lead to unclear and inconsistent claim decisions.

However, this policy provides a clear and detailed list of the exact diseases and procedures covered under this waiting period, removing ambiguity and ensuring transparency. The policy has two premium levels- Tier 1 (higher premium) and Tier 2 (lower premium). If you live in a Tier 2 city and pay the lower premium, you can still get treated in a Tier 1 city without any co-payment.

Points to Consider Before Buying

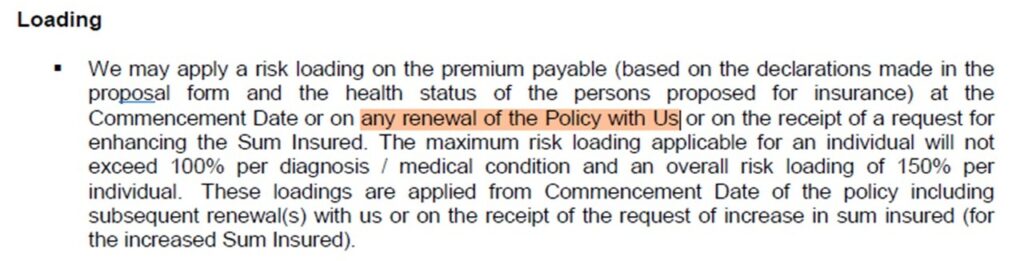

Energy policy terms mentions that risk loading on premium can be applied not only when you buy the policy or increase the cover but also at renewal. This seems unfair because, the insurer could use this to discourage customers from continuing the policy, especially if they consider them high-risk.

The waiting period for pre-existing diseases is 36 months. It is important to disclose all existing illnesses and adverse health conditions in the proposal form before purchasing the policy. HDFC ERGO reserves the right to either cover these conditions after the waiting period or permanently exclude them from the policy.

Policy mentions that claims under this policy will be serviced by the TPA. Generally HDFC Ergo settles all claims through its in house team.

If you get admitted to the hospital only to take certain injections in the joints or skin, or to receive special medicines like Zolendronic acid or IV immunoglobulin (IVIG), the policy will not cover such admissions.

The key features of the policy are summarised in the table below.

| Who can buy this policy | Person who are having – · Type 1 Diabetes, · Type 2 Diabetes Mellitus, · Impaired Fasting Glucose (IFG), · Impaired Glucose Tolerance (IGT) · and/or Hypertension |

| Hospital Room Entitlement | Private AC room |

| Cover limit you can choose | Rs. 200000; 300000; 500000; 1000000; 1500000; 2000000; 2500000; 5000000 |

| Pre and post hospitalisation cover | 30 and 60 Days respectively |

| Day Care | Covered |

| Organ Transplantation | Covered |

| Ambulance | Rs. 2000 per Hospitalisation. |

| Shared Accommodation Benefit | Eexclusions related to non-medical expenses shall be waived. |

| Restore benefit | 100% of cover limit restored if partially or fully exhausted. Restored cover limit can be used for any claim |

| HbA1C Checkup Benefit | 750 reimbursed for HbA1C test, with a maximum of two claims per policy year |

| Wellness Programme for Diabetes and Hypertension | Comprehensive programme with option to reduce renewal premium. |

| Cumulative Bonus | 10% enhancement of cover limit, maximum up to 100%, irrespective of claim in the policy. |

| Pre-existing Condition | 36 Months waiting period |

| Waiting period for specific listed diseases/procedures | 24 months |

| Pre- Acceptance Medical Test required | Yes |

| Loading on premium as per health status of person purchasing the policy | Yes applicable, 100% per diagnosis / medical condition and an overall risk loading of 150% per individual. · In First policy, · Increase in cover limit, and · On renewal |

Overall, HDFC Energy is a comprehensive health insurance plan designed for people with adverse health conditions such as diabetes and hypertension. Such individuals usually have very limited insurance options, and those available often come with many restrictions. This policy, however, offers broad coverage without unnecessary limitations, making it a strong option to consider if you need health insurance.